- Indians lost ₹22,495 crore to cyber fraud in 2025, with investment scams alone accounting for over 75% of that figure.

- Digital arrests and sextortion are now the fastest-growing fraud categories, and they're bleeding into the corporate world through employee targeting.

- iTechFixr's own VAPT engagements show Pune-Pimpri-Chinchwad SMEs are exposed at the same three points, every single time.

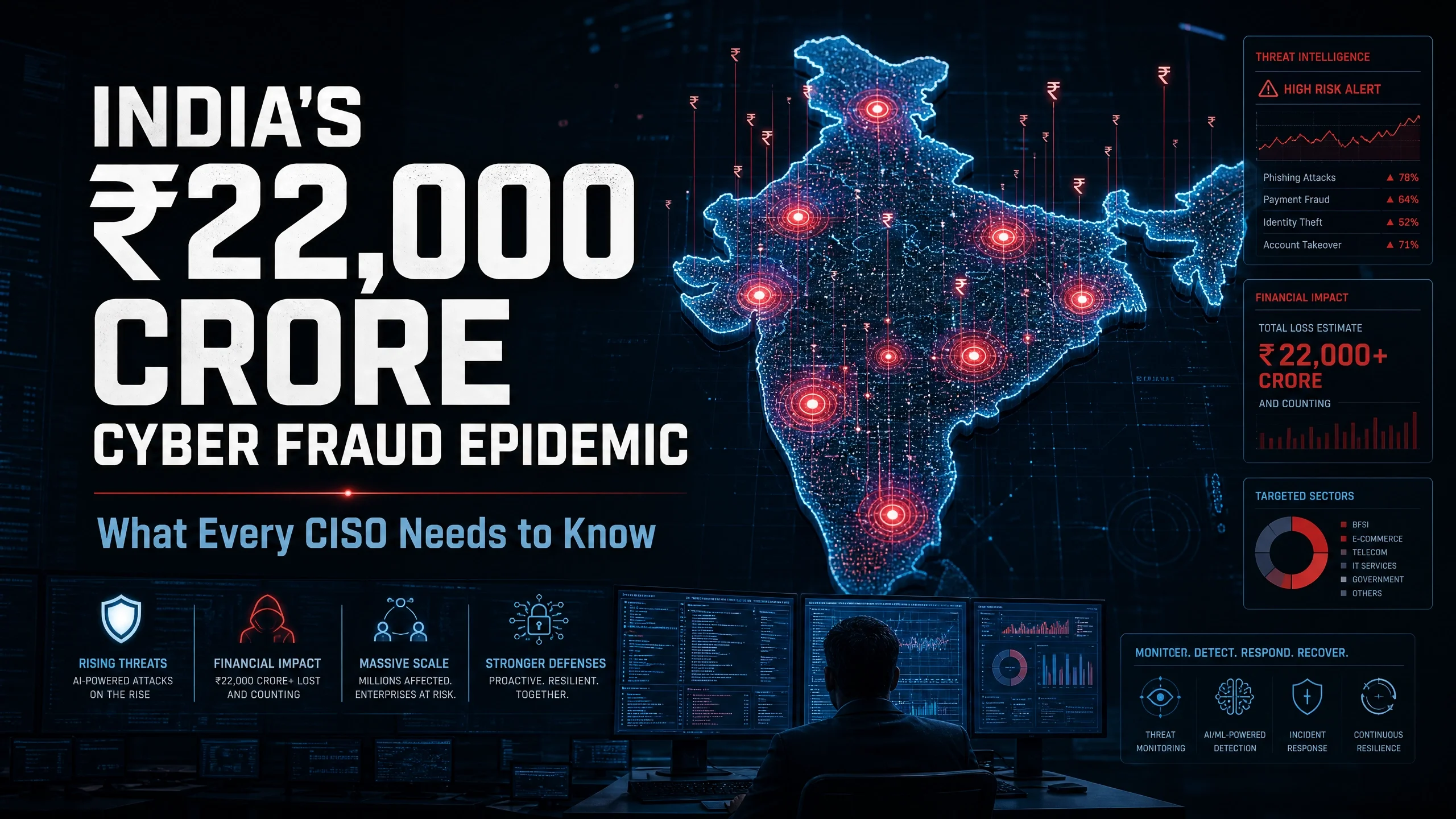

₹22,495 crore. That's what cyber fraud cost India in 2025 — against 28.15 lakh reported cases, a 24% jump from the year before. Investment scams alone swallowed more than three out of every four rupees lost. If you run a business in India and think this is a "consumer problem," you're reading the threat wrong.

Table of Contents

- How Big Is India's Cyber Fraud Problem, Really?

- Where Is the Money Actually Going?

- Why Are Businesses Getting Pulled Into Consumer-Style Scams?

- Key Takeaways

- Frequently Asked Questions

- How iTechFixr Can Help

How Big Is India's Cyber Fraud Problem, Really?

India lost ₹22,495 crore to cyber fraud in 2025 across 28.15 lakh registered complaints, per Ministry of Home Affairs data — and the real number is almost certainly far higher, since most victims never file a report.

The headline figure looks like it dipped slightly from ₹22,845 crore in 2024, but don't mistake that for progress. Case volume rose 24% in the same period. The dip in reported losses is largely down to faster fund-freezing by banks and the I4C's mule-account tracking, not fewer attacks. The Indian Cyber Crime Coordination Centre's own internal projection — based on early-2025 run-rate data — puts the *true* annualised loss closer to ₹1.2 lakh crore, nearly 0.7% of India's GDP, once unreported fraud is factored in. Only 55,484 of those 28.15 lakh complaints converted into FIRs in 2025, down from 66,370 in 2024 — not because crime fell, but because jurisdictional friction keeps most cases stuck at the reporting-portal stage. For a business owner, the lesson is blunt: the fraud you read about in the news is a fraction of what's actually happening, and the gap between "reported" and "real" is where your risk exposure quietly sits.

Where Is the Money Actually Going?

Investment fraud — fake trading apps, Ponzi schemes, and crypto traps — accounted for 76% of all financial losses in 2025, followed by digital arrest scams at 9% and sextortion at 4%.

These aren't random street-level scams anymore. The cases on record read like corporate fraud case files. A Hyderabad software engineer lost ₹3.2 crore to a fake trading platform discovered through a WhatsApp group — the fraudsters let him withdraw ₹10 lakh early specifically to build false confidence before stonewalling the rest. A Mumbai share trader with genuine market experience lost ₹86.9 lakh the same way; a fabricated dashboard showed his money "growing" to ₹2.1 crore. What connects these cases is patience — weeks of relationship-building before the ask. Banks have shared over 18.43 lakh suspect identifiers and 24.67 lakh mule accounts with the MHA's tracking registry, blocking ₹8,031 crore in fraudulent transactions since the system went live. That's real progress, but it also tells you the scale of the laundering infrastructure these networks run — multi-layered mule accounts moving stolen money across jurisdictions within minutes of a successful con.

Why Are Businesses Getting Pulled Into Consumer-Style Scams?

Digital arrest and impersonation scams increasingly target professionals at their workplace — doctors, bankers, retired executives, and senior staff — because their access to company funds and credentials makes a successful con far more valuable than a single consumer payout.

Parliament was told that digital arrest cases ballooned from 39,925 in 2022 to 123,672 by 2024, with losses crossing ₹1,935 crore. The victims documented in these cases aren't naive: a Ludhiana industrialist transferred ₹7 crore before realising it was fake, a Delhi doctor couple lost ₹15 crore to fabricated legal threats. In our own VAPT and awareness engagements across Pimpri-Chinchwad, the pattern repeats at the SME level — finance staff are the most-targeted role, not the owner, because they have transaction authority but rarely have the same scrutiny applied to their inboxes and calls. iTechFixr Infotech LLP has flagged this exact targeting gap in three separate client audits this year alone: finance teams trained on phishing emails, untrained on impersonation phone calls. That's the blind spot attackers are walking through.

Key Takeaways

- Treat "digital arrest" and impersonation calls as a business risk, not just a personal-safety topic — brief your finance and senior staff specifically.

- Don't measure your exposure by reported fraud numbers; the I4C's own estimate suggests real losses run five times higher than what's officially recorded.

- Audit who in your organisation has transfer authority and verify their training covers voice/video impersonation, not just email phishing.

- Use the 1930 cybercrime helpline and report immediately — early reporting is the single biggest lever in fund recovery right now.

Frequently Asked Questions

Q: Is India's cyber fraud problem actually getting worse or better?

A: Both, depending on what you measure. Reported financial losses dipped marginally in 2025 due to faster bank intervention, but case volume rose 24% and I4C's internal projections suggest true losses are roughly five times the official figure. For businesses, the honest read is: worse, not better.

Q: Why are digital arrest scams relevant to my business, not just individuals?

A: Because the same playbook — building false urgency and legitimacy over a call — is now being used against employees with company transfer authority. iTechFixr has seen this directly in client engagements: it's a corporate fraud vector wearing a consumer-scam disguise.

Q: What's the single biggest gap iTechFixr sees in SME cybersecurity audits?

A: Finance and operations staff are trained against phishing emails but rarely against voice or video impersonation calls. Attackers have noticed the same gap — Hardik Patel, CEH-certified cybersecurity trainer at iTechFixr Infotech LLP, Pimpri-Chinchwad, flags this as the most common finding across recent audits.

How iTechFixr Can Help

If you don't know where your business is exposed to fraud like this, you're guessing — and guessing is expensive. A VAPT audit from iTechFixr maps exactly where your people, processes, and systems would fail under a real attack, before someone else finds out for you.